What is Car Leasing?

Leasing – where you effectively agree a long-term rental of a car – is one of the cheapest ways to get into a brand-new car

Want a simple, low-cost way to get behind the wheel of a brand-new car? Car leasing - also known as Personal Contract Hire - could be the ideal choice.

Car leasing provides one of the lowest rates of monthly payment and is an uncomplicated way to pay for the use of a brand-new car. If you're looking for a used car, there are also leasing options available.

As a basic concept, car leasing is really nothing more complicated than the long-term rental of a car. All you do is pay an initial fee (usually equivalent to a set number of monthly payments) and then a series of fixed payments over an agreed period of time - there’s nothing more to it.

While private individuals can take out leasing agreements, businesses, sole traders and partnerships can access business leasing (which feature prices without VAT). Leasing is available for cars, vans and even taxis, but is typically restricted to new vehicles. The vehicle always remains the property of the leasing company.

Your complete guide to car finance

Car leasing pros

✔ Low, fixed payments for the latest cars

✔ You’re not liable for any unexpected drop in car’s value

✔ Easy to regularly upgrade to a new car

Car leasing cons

✘ Mainly limited to new cars

✘ Damage and excess mileage charges apply

✘ There’s no option to own the car

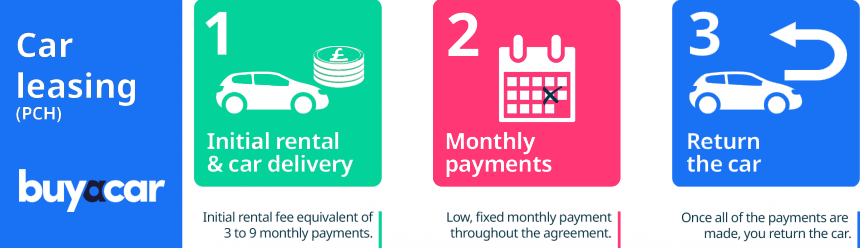

Car leasing - how it works

1. Choose your car and pay an initial rental fee, which is usually the equivalent of three, six or nine months of payments.

2. Your car is delivered and you'll make fixed monthly payments for the rest if the agreement

3. Return the car at the end. If you've exceeded the agreed mileage, or the car has damage, you'll be charged more.

What happens at the end of a car lease?

At the end of the term of your lease, you hand the car back, but there is no option to buy it. Part of a lease agreement will include a mileage limit.

Generally speaking, the higher the mileage you expect to do, the more expensive the lease, as higher-mile cars are worth less to the leasing company when they get them back. If you do go over this, you'll be charged a fee for every extra mile you cover. This is usually around 5-10p per mile, though with rare cars or some sports cars this could be as much as 30p or more.

You also need to return the car with nothing more than fair wear and tear or face extra charges.

If you want to purchase the vehicle at the end of the agreement it may be worth considering a PCP (Personal Contract Purchase). At the end of a PCP agreement, you have the option of buying the vehicle, although monthly payments are typically a little higher, like-for-like, than with a lease.

Car leasing: extra charges

After up to four years of driving, your leasing company won’t expect the car to be returned in the brand new, sparkling condition that it arrived in: stone chips and small scratches are expected.

These are assessed according to industry guidelines set out by the British Vehicle Rental and Leasing Association (BVRLA). These state, for example, that small scratches up to 25mm are usually acceptable, providing that they don’t go down to the base layer of the paint. Full details of acceptable defects will be available from your leasing company.

You’ll also be liable for extra charges if you drive beyond your mileage allowance, as higher-mileage cars are generally worth less. It’s common to pay for every mile you go over the limit.

How to get the cheapest lease deals

There is some flexibility in lease agreements, so they can be tailored to suit your needs. If you’re looking for the lowest possible monthly price, then you can reduce the mileage limit. The car will be worth more at the end if it has covered fewer miles, so leasing firms will charge you less.

Changing the length of the agreement will also affect the amount that you pay, but this will depend on the vehicle and how quickly it loses value.

In some cases, you’ll pay less each month for a longer, four-year agreement, (although you’ll be paying more overall). In others, the cheapest option is the shortest one - typically two years. Agreeing to make a larger initial payment will also reduce the monthly cost.

As with other types of finance, the cheapest lease deals are available on the least expensive cars and the ones that lose their value slowly.

Car leasing with low deposit

We don't offer leasing with no deposit here at BuyaCar but we do have a number of lease deals with only one or two months' worth of upfront payment needed that could fit the bill.

Alternatively, you can take advantage of a no-deposit PCP finance deal that provides you with low monthly payments and added flexibility at the end of the contract.

Can you cancel a car leasing agreement early?

It may be possible to return your leased car early and end your agreement by paying a settlement fee but this isn’t guaranteed. In some cases, you may even be asked to make all of your remaining monthly payments before you’ll be released from the contract.

You may get a more favourable option if you ask the leasing company to switch your lease to another vehicle - a larger, or more economical car, for example. However, there’s no guarantee that the request will be accepted.

In both cases, there's no harm in checking to see if a favourable option is available, but it’s best to assume that you’ll have to pay the full amount that you owe.

This does mean that it's even more important to ensure that payments are affordable before you start. However, leasing firms do know that circumstances sometimes change unavoidably, so it's important to get in touch with them if your payments suddenly become unmanageable.

Other car finance options

Hire Purchase is likely to be cheaper overall if you want to own a car outright. This is because the monthly payments are larger, meaning you're paying off the borrowing faster, reducing the cost of interest. With Hire Purchase, you own the car at the end, so if you plan to sell it in the near future, you’ll get less back for it if it suddenly loses value.

PCP is the most common form of car finance and unlike leasing, gives you the option to buy the car at the end, although many people will trade in for a new model. Monthly PCP payments are usually higher, like for like, than leasing.